I’ve been following Berkshire Hathaway’s Warren Buffet’s annual ‘Letters to Shareholders‘ for a number of years now. Amongst other things, he avoided the 1999-2001 tech bubble, and predicted the crash of 2007-08. We were lucky enough to go see him in ‘person’ at the Berkshire Hathaway annual meeting last year. This year, we decided to watch his Q&A on livestream (through Yahoo! Finance). Below are some of my thoughts as the meeting progressed. The format is various people (analysts, journalists, and audience member, in that order) ask questions in rotation until time runs out. This goes from about 9:30 until 3:30 Central, with Warren Buffet and Charlie Munger (his longtime business partner) holding court.

********************************************************************

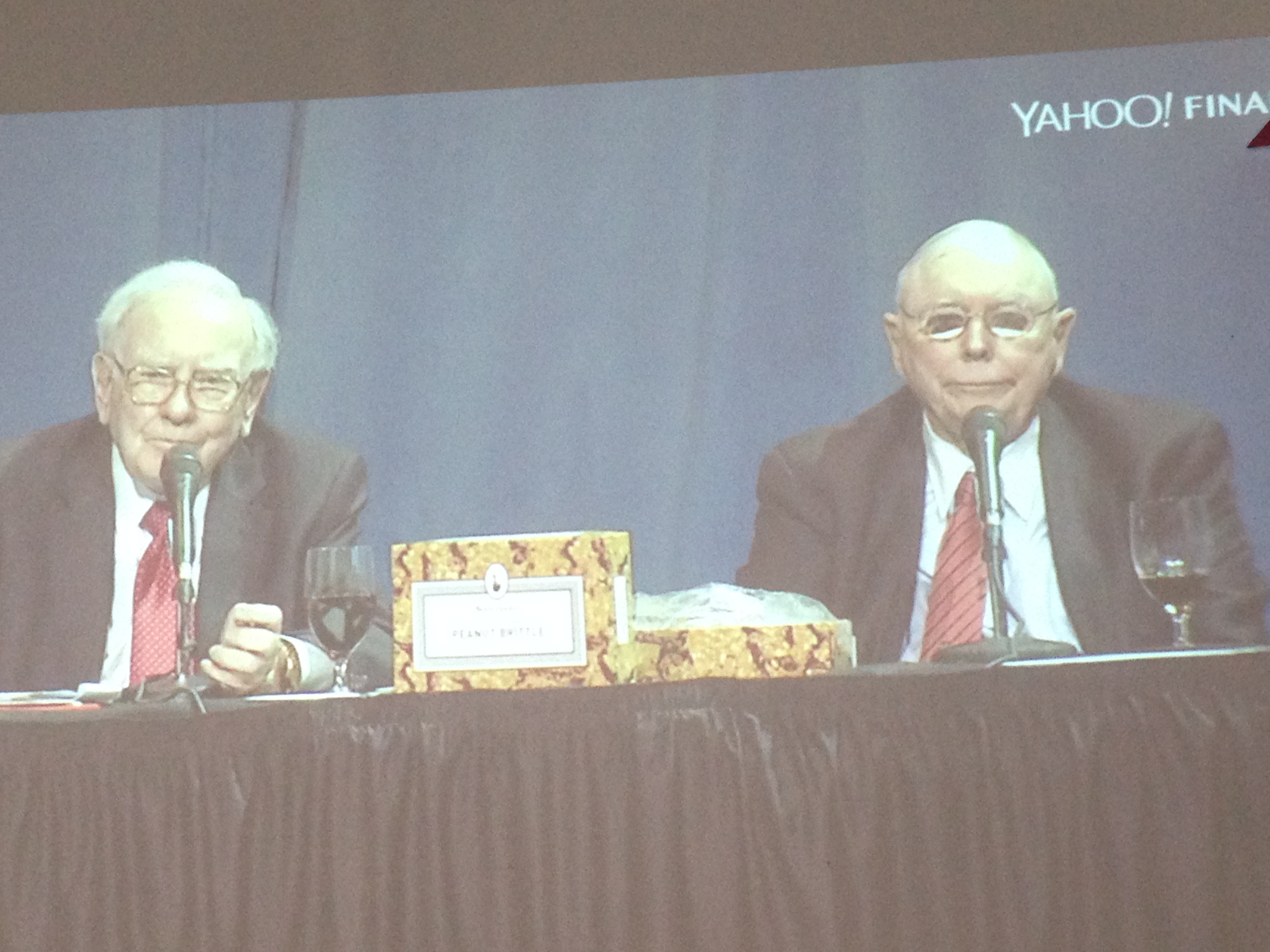

So again, we see the two (very) old friends up on the screen.

Q1: Going from low capital high earnings businesses to high capital moderate earnings businesses (regulated like rail and utilities).

The question asked why Berkshire moved from purchasing companies with low capital requirements and high income to purchasing companies with high capital requirements and moderate income.

The fundamental answer has to do with the size of opportunities available vs. the size of the conglomerate as a whole. (You can read all about it in the shareholder letters.)

Pithy remarks on the subject:

“Increasing capital acts as an anchor on earnings.”

This one I think was a Charlie-ism:

“When our circumstances changed, we changed our minds.”

Q2: Precision Cast, and the huge multiple premium paid

Under Berkshire, Helped make their main asset (the CEO) & made him more productive to the company.

Running a public company distracting vs. being under Berkshire.

“Buy a business that an idiot could manage, because eventually an idiot will have to.”

Q3: What would you do differently?

Warren said he’s ‘doing exactly what [they] like to do with the people [they] love’.

“It’s more fun to do things as a partnership.”

And a Charlie-ism:

“[Learning slowly] is a blessing too. At 92, I still have a lot of ignorance to work on.”

Q4: Munich and Swiss Re divestment

Business is less attractive for the next 10 years, because of low interest rates.

“Supply has gone up but demand has not gone up.”

“Reinsurance is easy to establish a disguised operation in a friendly tax jurisdiction. Couple that with low returns on float…”

Q5: Geico getting ‘whooped’ by Progressive Direct. Why?

Buffet: Diversion to number of car deaths/100M. From 1930 15/100M to 1/100M recently. (40,000)

‘Last year, for the first time, there was more driving, and more distracted driving’

‘Made a bet many years ago on the Geico model over the Progressive model.’

Charlie:

‘I don’t think we have to worry about a competitor having a good quarter.’

Q6: Direct sales -> Search, Push to Pull marketing…

Need to always think about the powerful trend (Amazon) when we make decisions.

‘Doesn’t worry us with Precision Cast.’

‘We were slow on the Internet.’ ‘Mobile and whatever.’

Internet still has much to change…

‘Thought of ourselves as having capital to allocate’, so makes it easier to pivot industries.

‘Amazon has a real advantage, 100s of millions of happy customers.’

Charlie

‘We failed so thoroughly at retail when we were young…[laughter]’ (so not likely to try retail again, and has helped guard them against that particular type of hubris)

Q7: Negative health effects of Coke products, why do you keep dodging the question?

[they dodged the question again]

184k deaths per year…’Declined to invest in cigarettes, why should be proud to own Coke?’

‘I’m about 1/4 coca cola. I’m not sure which quarter, I don’t know if we want to pursue that question.’

‘1.9 billion 8 oz servings per day.’ (Since 1886)

Dodged the question. ‘You have the choice of consuming more than you use.’ Talked about how Coca Cola is not the sole problem.

‘[small town with a constant population] Every time a girl had a baby, a guy had to leave town.’

‘If you want to change your longevity, you should have a sex change.’

Charlie:

‘We ought to almost have a law (I’m sounding like Donald Trump), that you have to say the benefits along with the detriments.’

Q8: Coal vs. renewables

Is your goal to get to 100% renewables?

‘We cannot make changes that are not approved by the Public Utility Commissions.’

‘Iowa’s been marvelous at encouraging renewables.’

In Iowa, we can offer lower rates because of it.

(2.3c/kWh federal tax credit)

‘Benefits of reducing carbon emissions are worldwide…’

‘A benefit that accrues to the world.’

Pay a lot of tax, so worth it to make a lot of investments

Iowa has gotten server farms because of cheaper electricity (from wind)

Vs. more expensive public Nebraska power…

Charlie:

‘If the whole rest of the world were behaving as we do, it would be a better world.’

‘I want to conserve the hydrocarbons’, for chemical feedstock…’I’m in their camp, for different reasons.’

Q9: Derivatives:

How do you value the banks you own?

‘If you asked me to describe the derivative position of the BoA…’

‘The great danger in derivatives is discontuinities’

WWI closed the stock market for many months

1987 almost did, but went on the next day

If marked to market and collateralized, most of the problems are okay…

Large quantities and collateral requirements are the most dangerous…

Kuwait went to a six-month stock settlement process, and caused all kinds of problems because of lack of certainty of ownership.

‘If you took the 50 largest banks, we wouldn’t look at [investing in] 45 of them.’

Charlie:

‘We’re in the awkward position of making 20B from those derivatives.’

‘We would have preferred if those derivatives had been illegal to buy. It would have been better for the country.’

One comment Buffet made which received less attention than it should have is about the issue with having an effective oligarchy amongst auditing firms. The specific issue was that the same person from an auditing firm could be rating or valuating the same derivative from both sides of the deal, and they could easily be rating or valuating it differently…

********************************************************

Those were the first 9 questions (out of a usual 60-ish). Stay tuned for more, comments below!

One thought on “Liveblogging the Berkshire Hathaway Annual Meeting”